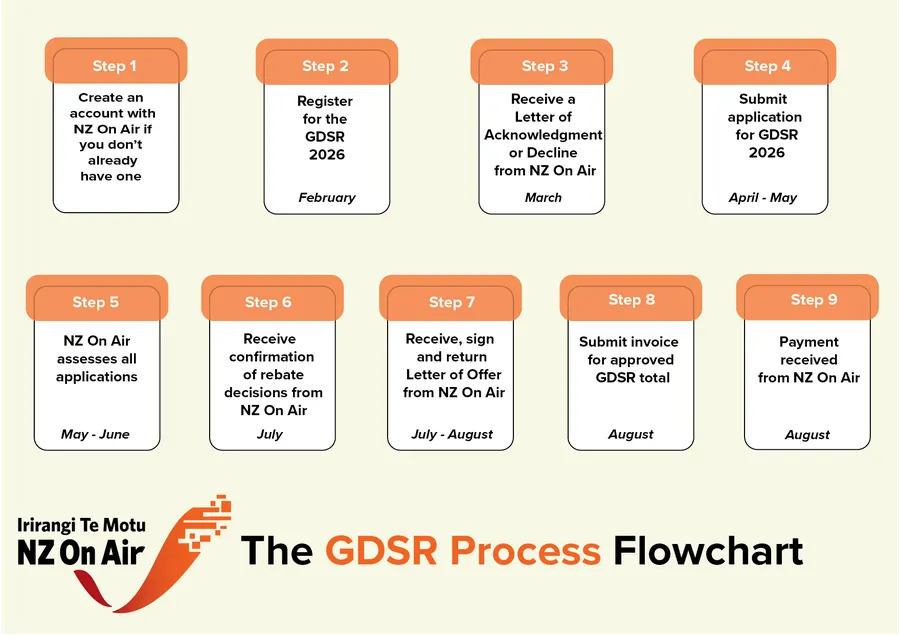

Did the Financial Details Template change in 2025?

Yes. In 2025, we used a mandatory template for the first time and overall received very positive feedback from applicants. For upcoming rounds, we have made a handful of further updates to the document aimed at providing additional context for applicants, and to improve the flow of application and assessment.

The Financial Details Template is designed to collect all the necessary information our financial assessors need in order to verify your claim and assess eligible expenditure, and ultimately streamline the assessment process.

What does paid (cash) or incurred (accrual) accounting mean, and how does it affect my application?

GDSR applications can be submitted using either a paid (cash) or an incurred (accrual) basis of accounting.

A paid (cash) basis means your accounting records income and expenses when money is actually received or paid. In other words, costs are counted at the time payment is made.

An incurred (accrual) basis records income and expenses when the economic benefit is received or the obligation arises, rather than when payment occurs. Costs are recognised over the period they relate to, providing a more accurate reflection of business expenditure and performance. For example, an annual software subscription may be paid upfront, but the cost would be recognised monthly across the year the service is used, rather than all at once at the time of payment.

For the GDSR, this means costs incurred must be allocated to the relevant eligibility period of 1 April to 31 March. If a software subscription period sits partly inside and partly outside that window - for example, an annual subscription running from February to February - you would only include the portion of the cost that relates to the months within the eligibility period. The remaining portion would be excluded or included in the following year’s application, as appropriate.

The method used must be declared at the start of the application and future applications should be consistent with that chosen approach. The method must also align with the basis used for reporting to Inland Revenue.

For more on this topic, you can find a helpful resource here from Xero: Cash accounting vs accrual accounting: Key differences explained | Xero NZ

On the Financial Details Template’s ‘eligible expense calculation’ tab, can we list a total amount per software or does each transaction need to be listed in a separate line?

We ask that you include a single line for each transaction, so that our financial assessors can confirm consistency with the data exported from your accounting system, and to break down those costs by transaction if needed. This means that a monthly subscription for a software-as-a-service would likely feature 12 individual lines for each monthly transaction.

Should ineligible expenses be included in the Financial Details Template?

Generally speaking, no. We only need eligible expenditure listed on the eligible expense calculation tab of the Financial Details Template. However, ineligible expenditure still needs to show up on your payroll export and reconcile with the amounts shown in your P&L. If you are unsure whether a cost is eligible, we recommend including it on the expense calculation tab. Our assessors will review every line on this tab and consider any edge cases, so some items you are unsure about may still be accepted, even if you have flagged them as potentially ineligible.

As ACC levies are billed as a lump sum and not broken down by employee, how should they be reported in the Financial Details Template?

If your ACC levies are as a lump sum, we accept a percentage of that lump sum payment equal to the percentage of eligible employee wages. This percentage is reached by looking at the amount of eligible salary (from your salary expense tab) divided by total salary.

Even if similar costs, such as KiwiSaver contributions, bonuses or benefits are calculated automatically through your payroll system, you’ll still need to manually enter the appropriate expenditure and percentages per employee in the ‘Employee and Contractor Calc’ tab of the Financial Details Template as this helps our assessors review your claim more accurately.

How do we treat depreciation when it comes to development expenditure?

Depreciation or amortisation of game development software and hardware is considered eligible expenditure.

If you have capitalised payroll or contractor costs related to Research & Development (R&D), these are only eligible if the actual costs were incurred during the tax year relevant to the rebate claim. However, amortisation of these capitalised costs is not eligible.

For clarity, depreciation on assets other than game development software and hardware is not eligible expenditure.

Any depreciation items must be included in your business' depreciation schedule, even low value assets that can be depreciated fully in any given year.

What counts as Research & Development (R&D) compared to game development - and how do we split this out?

We don’t require a distinction between R&D and game development for the GDSR — both are considered eligible activities.

However, if you’ve received other government funding (such as the R&D Tax Incentive), you must exclude any costs covered by those programmes from your GDSR claim. This is to avoid ‘double dipping’ – claiming the same expenditure under multiple government programmes – which is not allowed.

To ensure compliance, make sure any overlapping costs are identified and, if possible, removed from your GDSR claim. If you’ve removed those costs from the Financial Details Template, feel free to leave a note next to the declared RDTI entry to let us know they’ve been accounted for.

What documentation could an applicant provide to prove their employees or contractors are tax residents of New Zealand?

We don’t require applicants to provide proof that employees or contractors are tax residents of New Zealand.

Instead, we ask that you identify any employees or contractors who are not domiciled in Aotearoa New Zealand in your application.

Please note, a more detailed review may be conducted if your business is selected for audit. Each year, we carry out a random audit of 20% of successful GDSR applicants. If selected, we’ll contact you directly to explain the audit process and any further documentation required.

If a Registered Business applies for the GDSR and other government grants - such as the Research and Development Tax Incentive (RDTI), Centre of Digital Excellence (CODE) or a NZ Film Commission (NZFC) grant - at the same time, but the other grants have not yet been approved at the time the GDSR is approved, do they need to advise NZ On Air?

Yes. It’s important to let us know if you have applied for other government funding, even if it hasn’t been approved yet. You should provide details of the grant(s) and the amount applied for.

This allows us to understand that your GDSR application may be subject to change and ensures transparency about any potential adjustments.

Crucially, this requirement only applies where the other grant(s) relates to the same cost base — meaning the same expenses or the same eligibility period as your GDSR claim. The GDSR can only be claimed on eligible expenditure not already covered by another government grant, to avoid double dipping.

If the other funding relates to costs that fall outside the current GDSR eligibility period - for example, costs that sit within the next financial year - you would declare that funding in the relevant future GDSR application instead.

Does a Registered Business need to advise NZ On Air if they receive other government grants if the grant is unrelated to the GDSR, such as the Māori

Business Growth Support grant for example?

No, we only need to be advised if there is any crossover in relation to the eligible expenditure that is being claimed. If you are at all unsure, please get in touch with us (gamesrebate@nzonair.govt.nz) and we’ll be happy to help.

Is a Registered Business required to engage with a specific accounting firm for the audited accounts?

No, you don’t need to engage a specific accounting firm. If your application is selected for audit, NZ On Air will appoint an independent assurance provider to carry out the review. Our assurance provider will work directly with your finance team or your preferred accountant to complete the process. If your business is selected, we’ll get in touch to step you through what’s involved and answer any questions you might have.

What could a registered business expect from an audit if they are selected? Who conducts the audit and how are businesses selected?

Each year, NZ On Air audits a selection of GDSR recipients. Recipients may be chosen in one of two ways: either through a spot audit at NZ On Air’s discretion or through a random selection process of 20 percent of recipients. In either case, the audit is conducted at NZ On Air’s cost.

If your business is selected, we will contact you - typically around August - to let you know and answer any questions you may have. We’ll also provide a timeframe for the audit, which is usually expected to be completed within three months.

We’ll begin with an onboarding call to walk you through the process and introduce you to the independent assurance provider and relevant team members. The assurance provider will then liaise directly with your finance team or preferred accountant to arrange the review within the agreed timeframe.

As part of the audit, the assurance provider will select a sample of the eligible expenditure your business received the GDSR for. You’ll then have time to gather supporting documentation for those selected items.

This documentation might include:

- Invoices for software expenses

- Employment agreements for your New Zealand-based employees and contractors

- Timesheets or project time-tracking records for certain roles not typically involved in game development, such as a CEO, if time has been claimed for game development activities.

The assurance provider may request further details as needed. NZ On Air will remain available throughout to help guide you through the process and ensure everything runs as smoothly as possible.

Please note, having been audited previously does not exclude a business from being chosen for audit again in the following year(s).

How should a company apportion costs if their year-end is not 31 March (e.g. year-end is 1 Jan to 31 Dec)?

When you are registering for the GDSR, projections for expenditure based on rationale are acceptable. However, please note that in your GDSR application, figures provided must be based on actual expenditure for the eligibility period 1 April-31 March.

If a group has multiple entities in New Zealand, which entity should make the claim? i.e. the top holding company in New Zealand? The entity that holds the IP? The entity that incurs the salary costs? And what if the salary costs are re-charged to another entity?

The key consideration here is to ensure there is no double dipping in expenses across multiple applications and to direct the rebate to the businesses in line with the policy intent of the GDSR. Conceptually, this points to the claimant as a game development studio and not its contractors. It also points to the claimant as a self-standing studio with a Company Number and all other factors of eligibility, and not a holding company that has no eligible game development activity of its own. With that in mind, the entity which should make the claim would be the entity incurring the salary cost, which may also hold the IP.

Should costs be submitted including or excluding GST?

All costs must be submitted excluding GST.

Please note that some international suppliers do not charge GST. In these cases, you should submit the full invoice amount as shown. Take care not to deduct 15 percent from overseas invoices that do not include GST.